@media (max-width: 600px) {

.ib-container h2 { font-size: 30px !important; }

.ib-container p.main-text { font-size: 26px !important; }

.ib-container p.sub-text { font-size: 20px !important; }

.ib-container a { font-size: 18px !important; padding: 12px 26px !important; }

.ib-container { padding: 24px !important; }

}

Interactive Brokers

More markets than any other platform.

Over 150 markets available for Canadians

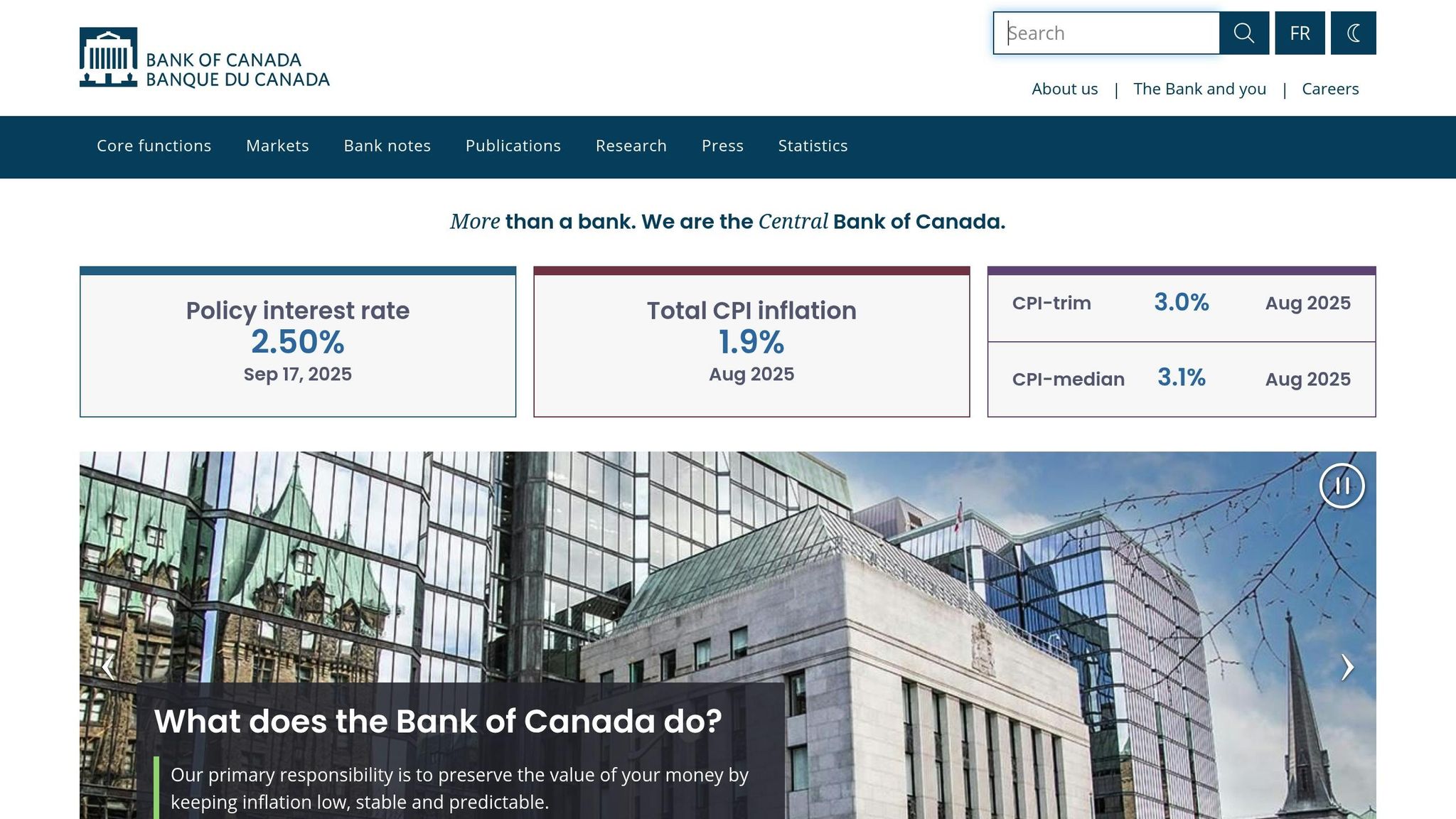

Interest rate changes in Canada are reshaping decisions around homeownership, renting, and mortgages. The Bank of Canada has reduced its policy rate to 2.50% (from a peak of 5.0% in 2024), but borrowing costs remain higher than pre-pandemic levels. Here’s what you need to know:

- Higher Mortgage Costs: Fixed and variable-rate mortgages are pricier, with monthly payments up significantly compared to a few years ago.

- Renting vs Buying: Renting is often more affordable in the short term, but buying offers long-term stability if costs align with your budget.

- Mortgage Renewals: Many homeowners face “renewal shock”, with payments jumping by $1,000+ per month in some cases. Options like extending amortization or switching rates can help.

- Future Rate Outlook: A potential rate cut is expected by the end of October 2025, but long-term forecasts suggest rates could rise again in 2026–2027.

Navigating today’s housing market requires careful planning. Whether you’re buying, renting, or renewing, understanding the financial impact of interest rates is key to making informed decisions.

Why Are Mortgage Rates Rising as the Bank of Canada Cuts Rates?

Canadian Mortgage Rates Today

As interest rate changes continue to influence housing decisions across Canada, staying informed about current mortgage rates is crucial. These rates are shaped by the Bank of Canada’s policies and broader economic trends. Here’s a closer look at where things stand today and what factors are at play.

As of September 2025, the Bank of Canada’s policy rate is 2.50%, a drop from its peak of 5.0% in June 2024. This shift has brought the bank prime rate down to 4.70% [1][2][3]. While this reduction has eased borrowing costs, the future direction of rates remains uncertain, with economic signals painting a mixed picture.

Economic data reveals a complex landscape. Headline inflation rose slightly to 1.9% in August 2025, up from 1.7% in July, though it remains just below the Bank’s 2.0% target [1][2]. Meanwhile, core inflation persists at a higher level of 3.05% [1][2]. On the employment front, the labour market added 60,000 jobs in September, particularly in manufacturing, while the unemployment rate held steady at 7.1% [1]. These factors all play a role in how lenders determine their mortgage rates.

Fixed vs Variable Rate Comparison

Deciding between fixed and variable mortgage rates has become more challenging in today’s shifting market. Variable rates tend to follow the Bank of Canada’s policy rate, while fixed rates are influenced by bond market trends and lender competition.

At the moment, the Canadian 5-year bond yield is around 2.7% [1], serving as a key benchmark for fixed-rate mortgages. If you believe further rate cuts are likely, opting for a variable rate may be the way to go. On the other hand, if you prefer the stability of predictable payments, a fixed rate might be a better fit.

Understanding these dynamics can help you make a more informed choice, but what about the future of these rates?

Rate Predictions for the Next 2 Years

Looking ahead, market expectations for the Bank of Canada’s next decision on October 29, 2025, suggest a 55% chance of a 25-basis-point cut and a 45% chance of no change [1]. With the Bank’s neutral rate range estimated between 2.25% and 3.25% [1], the current policy rate of 2.50% sits near the middle of this range. This means there’s limited room for further cuts without entering a more stimulative phase.

Geopolitical factors are also adding uncertainty. For example, U.S. trade policies, including the risk of tariffs and government shutdowns, are creating mixed signals for inflation and economic growth. According to National Bank, 36% of Canadian businesses have been impacted by the ongoing trade conflict [1], illustrating how external pressures can influence domestic monetary policy.

Beyond 2025, many economists anticipate a shift away from the current easing cycle. Some forecasts suggest that rates could climb again in 2026–2027 as economic conditions stabilize and inflationary pressures resurface. Over the long term, interest rates are expected to settle higher than the historically low levels seen between 2008 and 2020. Factors like deglobalization and protectionist policies are contributing to this trend, keeping average interest rates elevated compared to the previous decade.

For those making housing decisions, today’s rates might represent a balanced opportunity. While they are higher than the ultra-low rates of recent years, waiting for further reductions could backfire if rates rise as predicted. These patterns should be a key consideration in shaping your housing strategy.

Can You Afford a Mortgage Right Now?

With current interest rates and an economy that keeps shifting, figuring out if you can afford a mortgage requires more than just looking at how much you can borrow. It’s about understanding what you can comfortably handle financially, month after month, without stretching yourself too thin.

How to Calculate Your Mortgage Payments

To get a clear idea of what your mortgage payments might look like, you need to break them down into their key parts. These include the principal (the loan amount), interest, property taxes, and home insurance – collectively known as PITI. If your down payment is less than 20%, lenders will also likely require you to take out mortgage insurance, which adds to your costs.

Online mortgage calculators can give you a quick estimate of your payments. These tools let you adjust variables like interest rates, amortization periods, and down payment amounts to see how they influence your monthly obligations.

For instance, let’s say you’re looking at a $500,000 home and plan to put down 10% ($50,000). That leaves you with a $450,000 mortgage. At a 5.5% interest rate for a 5-year fixed term with a 25-year amortization, your monthly payment would be about $2,740. If the rate dropped to 4.5%, your payment would decrease to roughly $2,510, saving you $230 each month.

If you extended the amortization period from 25 to 30 years, your monthly payment would drop further – from $2,740 to about $2,560. However, this would come at a cost: you’d pay an additional $63,000 in interest over the life of the loan.

The Canadian Mortgage Stress Test Explained

After estimating your mortgage payments, you’ll need to consider Canada’s mandatory mortgage stress test. This test ensures you can handle payments even if interest rates go up, protecting both you and your lender from potential financial strain. To pass, you must qualify at the higher of two rates: either the Bank of Canada’s 5-year benchmark rate or your contract rate plus 2%.

Using the earlier example, while your estimated payment at 4.5% might be $2,510 monthly, the stress test could require you to qualify based on payments closer to $2,740. If your gross monthly income is $8,000, your housing costs should generally stay within 32% of that amount, and your total debt obligations shouldn’t exceed 40%.

The stress test has become more challenging as rates have climbed from the historic lows of 2020 and 2021. Back then, when rates hovered around 1–2%, qualifying was much easier. Now, many Canadians find themselves unable to meet the stricter requirements, even though today’s rates are still moderate compared to older historical averages.

Mortgage Renewal Challenges

Affording a mortgage isn’t just about the initial purchase – it’s also about managing it when it’s time to renew. Many homeowners are facing “renewal shock” as rates reset, requiring careful planning to adjust their budgets.

Take, for example, someone who took out a $400,000 mortgage in 2021 at a 1.8% interest rate with a 25-year amortization. Their monthly payment was around $1,720. Fast forward to today, and renewing that mortgage at 5.5% with 20 years left would push their payment to about $2,750 – an increase of over $1,000 per month, or $12,000 annually.

There are ways to ease this transition. Extending your amortization back to 25 or 30 years can lower monthly payments, though it means paying more interest over time. Some lenders offer programs that gradually increase payments over a year or two, softening the immediate impact.

Switching to a variable rate might also offer temporary relief if you believe rates will drop, but it’s a gamble – if rates rise, you could end up paying more. Another option is making a lump sum payment toward your mortgage principal before renewal. This reduces your balance and, in turn, your monthly payments.

If you’re unable to qualify for a renewal with a new lender, staying with your current lender can help you avoid another stress test. However, switching lenders would trigger the test, potentially limiting your options.

To prepare for renewal, start discussions with your lender 4–6 months before your term ends. This gives you time to explore your options, negotiate better rates, and plan for higher payments without feeling rushed into a decision.

sbb-itb-24a3f88

How to Handle Higher Housing Costs

As interest rates shift across Canada, housing costs are becoming a bigger piece of the financial puzzle. If you’re feeling the squeeze, it’s time to revisit your financial plan. By reassessing your mortgage options, tweaking your budget, and tapping into Canadian financial tools, you can keep your homeownership goals steady despite rising costs.

When to Refinance or Change Your Mortgage Rate

Refinancing could make sense if you can lock in a much lower interest rate and plan to stay in your home for several years. But keep an eye on potential costs, like prepayment penalties, if you’re breaking your current mortgage early. If you’re locked into a high fixed rate, switching to a variable rate at renewal might offer some relief. Struggling at renewal time? Talk to your lender and see if they’ll offer loyalty discounts or improved terms. This could save you from going through the additional qualification process. Another option to consider is a collateral charge mortgage, which allows more flexibility in accessing your home equity. These strategies can help you manage rising payments and stay on top of your finances.

Adjusting Your Budget for Increased Payments

After sorting out your mortgage strategy, the next step is to adjust your budget to accommodate higher payments. Start by trimming non-essential expenses – think dining out, streaming subscriptions, or other discretionary spending. Reorganize your budget to focus on covering your mortgage and other essentials while still setting aside savings for the future. You might also explore bi-weekly payments to improve cash flow and reduce interest over time. Adding occasional extra payments toward your principal is another way to ease the burden of rising costs in the long run.

Leveraging Canadian Financial Tools and Resources

To complement your mortgage and budgeting efforts, take advantage of the financial resources available in Canada. Websites like Wealth Awesome offer tailored advice, mortgage calculators, and comparison tools to help you explore options like extra payments or switching between fixed and variable rates. Mortgage brokers can also be a valuable resource, often providing access to preferential rates and expert insights. Don’t overlook credit unions, which may offer more flexible lending terms and financial counselling services. Additionally, the Canada Mortgage and Housing Corporation (CMHC) offers programs designed to support homeowners. For a more personalized approach, fee-only financial planners can help you fine-tune your mortgage, tax, and investment strategies, ensuring your finances are optimized for the current housing market challenges.

Other Housing Options Besides Buying

With rising interest rates making traditional mortgages less appealing, many Canadians are exploring alternative housing strategies. These options can provide more financial flexibility and lower upfront costs compared to conventional homeownership. Let’s take a closer look at how renting compares to buying in today’s market and explore some innovative housing solutions.

Renting vs Buying in Today’s Market

Higher interest rates have dramatically altered the financial equation between renting and buying. In many parts of Canada, renting has become a more affordable option in the short term compared to taking on a high-interest mortgage.

| Advantages of Renting | Advantages of Buying |

|---|---|

| Lower monthly expenses | Opportunity to build equity over time |

| No responsibility for maintenance or repairs | Stability and control over your living space |

| Flexibility to move without selling a home | Potential tax benefits and deductions |

| No need for a large down payment | Protection from rising rents |

| Predictable monthly costs | Freedom to renovate and personalize your property |

These factors can help you determine which option aligns better with your current financial and lifestyle needs.

When Renting Makes Sense: Renting is often the better choice if mortgage payments would consume more than 35% of your gross income or if you anticipate moving within the next five years. The savings from renting can be redirected toward building a larger down payment or investing in other opportunities.

When Buying Is a Good Option: Buying can still be a smart move if the total cost of ownership (including taxes, insurance, and maintenance) is comparable to rent in your area, and you plan to stay in the home for at least seven years. Over time, this stability can help you build equity even in a high-rate environment.

Creative Housing Solutions

Beyond the traditional rent-or-buy debate, Canadians are turning to creative housing arrangements to navigate today’s affordability challenges. These strategies are helping many find stable housing without overextending their budgets.

Co-ownership and Shared Ownership: This involves multiple parties purchasing a property together or participating in housing cooperatives. Families, friends, or even strangers (through specialized platforms) can pool resources to share down payments and ongoing costs. Each party owns a percentage of the property, with shared expenses like mortgage payments and maintenance divided accordingly.

Multi-generational Living: More families are opting for multi-generational homes, where adult children stay with parents longer, or elderly parents move in with their adult children. This approach can reduce housing costs while providing mutual support. Some families are even renovating their homes to create separate living spaces or seeking properties with secondary suites.

Rent-to-Own Programs: These arrangements allow renters to work toward homeownership by paying above-market rent, with a portion of the payment going toward a future down payment. While not widely available in Canada, some private companies and non-profits offer these programs, particularly targeting first-time buyers.

House Hacking: This strategy involves purchasing a property with multiple units, living in one, and renting out the others. For example, you could buy a duplex, triplex, or a home with a basement apartment. The rental income can help offset mortgage payments, making homeownership more affordable while you build equity.

While these solutions require careful financial planning and legal agreements, they offer practical ways for Canadians to secure housing in a challenging market. Whether through shared ownership, multi-generational living, or leveraging rental income, these strategies are reshaping the housing landscape.

Making Smart Housing Decisions in 2025

Navigating Canada’s housing market in 2025 means staying informed and keeping your strategy flexible. With affordability challenges and shifting market trends, the key to making confident housing decisions lies in consistently tracking market updates and relying on trusted Canadian resources.

For reliable insights, turn to official sources like CMHC, CREA (with their next update scheduled for January 15, 2026 [4]), Canadian Mortgage Professional [4], and True North Mortgage [5]. These platforms provide timely market intelligence and daily updates to help you stay ahead of changes.

Expert opinions also play a crucial role. Shaun Cathcart, CREA’s Senior Economist, shared in July 2025:

Markets appear to be entering their long-expected recovery phase, fuelled by pent-up demand, lower interest rates, and an economy that is expected to avoid worst-case tariff scenarios. [5]

For a broader perspective, review market analyses from CMHC, Oxford Economics, Royal LePage, TD Economics, Rosenberg Research, and PwC Canada [5][6]. These expert insights can help you make sense of the bigger picture and guide your decisions effectively.

When it comes to mortgages, professional advice is invaluable. Mortgage brokers can provide unbiased guidance on affordability strategies, whether you’re deciding between fixed and variable rates or weighing your options for mortgage renewal. Additionally, online tools like calculators and housing statistics platforms allow you to model different interest rate scenarios and see how they might impact your payments [5].

Flexibility is key in uncertain times. True North Mortgage underscores this point:

Home buyers aren’t likely to commit to a big home purchase or move if worried about their financial futures. Inflation uncertainty can moderate housing demand and put downward pressure on prices. [5]

To stay prepared, consider reviewing your financial situation every six months. Take stock of your affordability, assess current market conditions, and evaluate any changes in your personal circumstances.

Timing is also critical, especially with ongoing interest rate fluctuations. Some economists warn that unless the Bank of Canada implements deeper rate cuts, there could be a risk of further price declines. This makes careful planning essential.

Whether you’re aiming for traditional homeownership, exploring alternative housing options, or continuing to rent, success in 2025’s housing market depends on staying informed and adaptable. As the landscape evolves, a well-thought-out approach will help you navigate the challenges and opportunities ahead.

FAQs

How can Canadians prepare for higher mortgage payments when renewing their mortgage?

If your mortgage renewal is on the horizon, it’s wise to start planning early – ideally about four to six months before your term ends. This gives you time to evaluate your options and prepare for any potential changes in your payments due to higher interest rates.

Begin by using online mortgage calculators to get a sense of how increased rates might impact your monthly payments. This step can help you understand how these changes could fit into your overall budget.

Don’t just accept your current lender’s renewal offer without exploring alternatives. Take the time to compare rates from other lenders. You might find a better deal elsewhere. Additionally, options like extending your amortization period or tweaking your payment frequency could make your payments more manageable. However, keep in mind that these adjustments may result in paying more interest over the life of your mortgage.

For a more personalized approach, consider consulting a financial advisor. They can help you develop strategies tailored to your situation, such as refinancing or consolidating debt, to better handle rate increases. By planning ahead, you can ease the transition and maintain your financial stability.

What should Canadians consider when choosing between a fixed-rate and variable-rate mortgage in today’s market?

When choosing between a fixed-rate and a variable-rate mortgage in Canada, you’ll need to consider your financial priorities, comfort with risk, and the current interest rate trends.

A fixed-rate mortgage gives you the security of consistent payments, making it easier to plan your budget. However, this stability often comes with slightly higher rates compared to variable-rate options. On the flip side, variable-rate mortgages typically start with lower rates, offering potential savings, but your payments could fluctuate if interest rates change.

If you value predictable payments or are worried about rising rates, a fixed-rate mortgage might suit you best. But if you’re open to some uncertainty and believe rates may drop, a variable-rate mortgage could lead to savings. Not sure which way to go? A shorter-term fixed-rate mortgage might strike a balance, giving you time to reassess as the market shifts.

What are some affordable and creative housing options for Canadians impacted by rising interest rates?

For Canadians grappling with the increasing expenses of traditional homeownership, there are a few housing alternatives worth considering:

- Tiny homes: These compact, self-sufficient spaces are easier on the wallet when it comes to both buying and upkeep.

- Modular homes: Built in sections at an off-site location and then quickly assembled, these homes often come with a lower price tag.

- Shipping container homes: Old shipping containers can be creatively turned into affordable and distinctive living spaces.

These options provide a way to cut costs while offering flexible housing choices that align with shifting market demands.