Before we get to my economic and stock market predictions for 2026, I invite you to check out last week’s report column to see how I did in my 2025 predictions.

As usual, I’m going to offer a general disclaimer: This isn’t meant to be direct investment advice. It’s more for my own fun, with a dash of “see – I’m a credible financial thinker” ego management tossed in. Financial markets are influenced by far too many moving parts to be forecast with precision – especially over an arbitrary 365-day window. Interest rates, politics, investor psychology, inflation, technology, geopolitics… the list goes on and on. Change a single assumption and the entire forecast can change rapidly for a given year.

All of that said, I still think there’s value in doing this exercise. It forces us to think through economic pressures, incentives, and risks. It helps separate signal from noise. And, maybe most importantly, it gives long-term investors a framework for staying the course when headlines get sensationalistic.

What follows isn’t a list of bold click-baity calls, or market-timing advice. It’s a look at where economic pressures are building, where assumptions look stretched, and what key indicators I’m looking for in 2026.

The Battle of the Year: Trump vs Economic Gravity

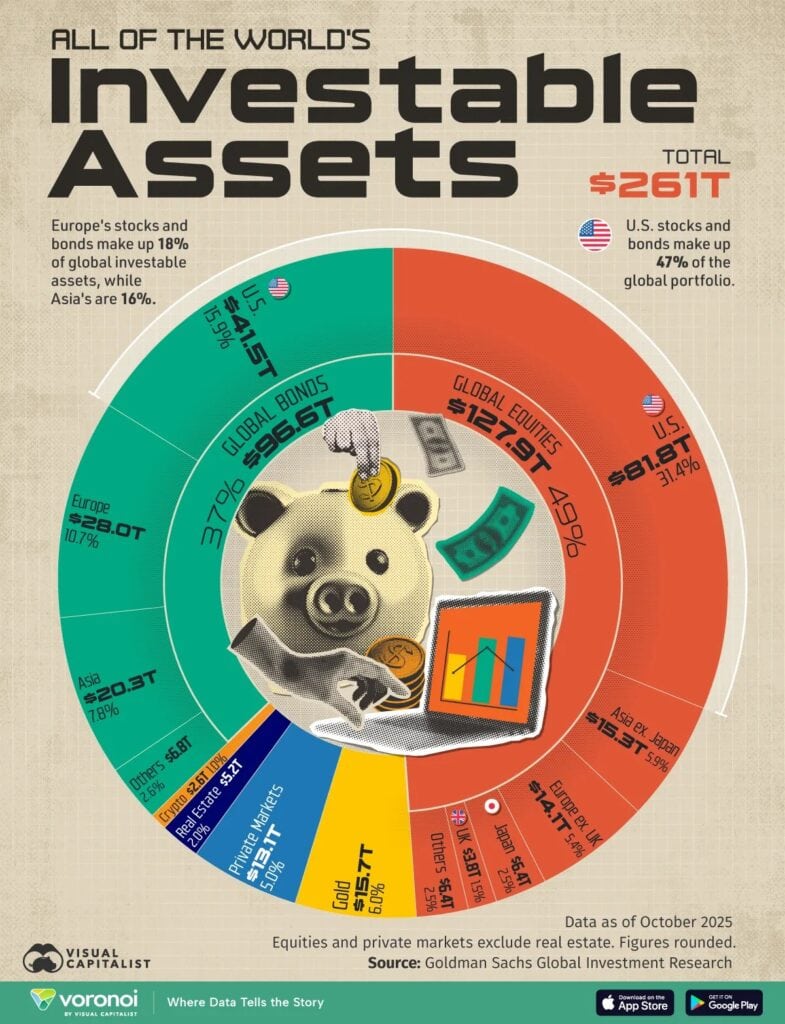

The US stock market has grown to a point where it just dominates the rest of the investable world. This recent Visual Capitalist post gives you some idea of that reality:

Consequently any discussion of where the world’s markets are headed in 2026 has to start with the USA…

I get a kick out of how often stock market conversations start with where prices are going and skip right past what’s already priced in.

That’s the real issue for U.S. stocks heading into 2026.

Valuations are high. Not “a bit above average” high – but high enough that there’s very little margin for error. When markets are priced for near-perfection, the upside usually depends on things getting even better. The downside can show up when reality just turns out to be… normal (or worse). I wrote about this in my recent AI bubble article.

That’s why trying to predict 2026 feels less like a straight-line forecast and more like a tug-of-war.

On one side, you’ve got political pressure actively trying to keep markets artificially-levitated as we head into the midterms. On the other, you’ve got economic forces that don’t care what any politician wants to happen.

President Trump has never been shy about his belief that rising markets equal economic success. Loose fiscal policy, pressure on central banks, and market-friendly messaging have always been central to his approach. There’s already evidence that this mindset is shaping expectations.

I think there is little doubt that Trump is going to continue to run huge deficits, and pressure the Federal Reserve to drop rates as low as possible. The more successful he is in doing those things, the more juice will be squeezed into asset prices. Stocks, gold, silver, everything should see a bounce.

However, at some point, economic gravity is bound to assert itself.

Tariffs, inflation expectations, and bond yields don’t respond to optimism or rhetoric.

Tariffs are inflationary by design. That’s not a partisan take – it’s basic economics. Economists across the spectrum have repeatedly noted that trade barriers raise input costs and consumer prices, even when exchange rates adjust.

If inflation remains sticky, the bond market reacts first. If you combine that with loose monetary policy, we could see inflation spike into the 4% territory. That pressure is going to reverberate in many directions, likely causing quantitative easing to pick up, and generally upsetting people who want lower inflation.

Analysts at JPMorgan Chase have warned that when equity valuations sit well above long-term averages, even modest increases in real yields can compress price-to-earnings multiples. You don’t need a recession. You don’t even need collapsing earnings. You just need expectations to cool.

Add in a decelerating U.S. economy – softer job growth, more cautious consumer spending, and increasingly careful corporate guidance – and the rope gets pulled tighter from both ends.

That’s the tug-of-war.

You don’t need to predict who “wins” this battle to understand the setup. When markets are priced for perfection, volatility tends to rise because there’s less cushion for disappointment. That doesn’t mean U.S. stocks collapse in 2026. It does mean returns are likely to be more sensitive to inflation data, bond yields, and policy surprises than they were when valuations were lower.

I don’t think there is going to be a clear winner in this dust-up, but as we go through the predictions below, keep in mind that this large macroeconomic battle is going to be going on in the background throughout 2026.

Stock Markets Finish the Year Flat

he last three years have seen incredible stock market returns in both Canada and the USA.

I’m predicting that there won’t be a 4-peat.

Both the TSX 60 and the S&P 500 will make a lot of market noise on their way to finishing somewhere in the neighborhood of up 5% or down 5%. That may not sound exciting, but it’s actually a pretty common outcome when starting valuations are elevated and economic signals are mixed. This is actually going out pretty far on a branch as the vast majority of publications are calling for another year of 10%+ gains.

In other words I think the tug of war I started this article with is going to see a lot of strong forces cancel each other.

I always start from the standpoint that roughly three-quarters of the time, the stock market will have a positive year. In other words, it pays to be an optimist. So what’s working against big gains this year?

Namely, just super high expectations that have been baked into very high stock market valuations. You don’t need a crash. You just need earnings growth that’s “good but not great” – and we could easily see a 30% drawdown just on that premise alone. Of course it could be similar to 2025 where we see a big drawdown followed by an even more dramatic rally.

Canada’s valuations aren’t quite as stretched as the US’s, but then again our economy isn’t as dynamic either. Compared to our long-term average, we’re still pretty highly valued. For example, RBC is a great company (and the second largest in Canada). Its price-to-earnings ratio usually sits around 9x-12x. Right now it’s 16.5x. So either RBC is going to grow profits WAY faster than it has in the past… or it’s a bit overvalued. Still a great company – but a bit overvalued.

At the same time, there are several good reasons why the stock market isn’t going to experience a “bubble pop”. Chief among them is that governments don’t want them to – and understand which levers to pull better than they did in the past.

Additionally, corporate balance sheets remain relatively healthy by historical standards. Analysts at Goldman Sachs have highlighted that outside of a few stressed pockets, companies still have manageable debt loads and access to financing. That reduces the odds of a cascading earnings collapse.

At the end of the day, it’s hard to predict where the exact number is going to fall 365 days from now, but I think the negative risks outweigh the positive possibilities at the moment – just not by much.

The TSX 60 and S&P 500 Will Each See a Big Dip

I’m predicting that the string of low volatility months is going to end. I just think it’s more probable than not that extreme emotions are going to happen because they’ve largely been held in check for a while now.

At some point in 2026, I expect the TSX 60 to be down roughly 20% from a recent peak, and the S&P 500 to be down closer to 25%. Not as part of some big financial apocalypse. Just… at some point during 2026.

That may sound extreme if your mental model of markets has been shaped by the unusually smooth ride we’ve had over the last 15 years. But historically speaking, this kind of drawdown is far more common than most investors remember. Over the last century, the U.S. stock market has experienced roughly 22 bear instances where there has been a decline of 20% or more from peak to trough. That works out to about once every 4.5 years on average.

Recent market history has conditioned investors to expect fast recoveries and relatively shallow pullbacks. When markets bounce back quickly a few times in a row, it starts to feel like that’s the default setting.

It isn’t.

When valuations are elevated, interest rates are higher than the post-2008 norm, and economic growth is slowing but not collapsing, markets become more sensitive to disappointment. Earnings misses matter more. Inflation surprises matter more. Bond yields can cause panic faster.

That’s when you tend to get sharp pullbacks that feel sudden, even though they fit perfectly within historical norms.

Obviously given that I expect the year to end up close to even, I expect a recovery of some kind as well.

It’s not just the tech companies that have high valuations. Wal-Mart, Costco, gold, silver, the list goes on and on. In order to keep going up steadily, everything will have to break absolutely perfect in the markets this year. Maybe it will (that’s certainly a possibility) but I think odds are there might be a wrench thrown into the mix somewhere. (China-Taiwan?)

The Canadian Dollar Will Be up vs the USD

I think the Canadian Dollar strengthens against the USD at some point in 2026 – not necessarily in a straight line, but enough that it’s noticeable (5-10%).

Here’s the basic idea. The Bank of Canada’s estimate for Canada’s nominal neutral rate is in a 2.25% to 3.25% range. Today, the Bank of Canada’s policy rate is already sitting at 2.25%. Our inflation rate is relatively close to our 2% target, and our unemployment rate is not spiralling. It appears that Canada has done most of the monetary and fiscal easing that it’s going to do for the time being.

The other side of the coin though is that Trump has been publicly pushing for substantially lower U.S. interest rates, and he’s been explicit that the next Fed chair should believe in cutting rates “by a lot” – potentially down toward 1%, versus the current fed funds range of 3.5% to 3.75%.

Whether Trump will fully get what he wants, the direction of pressure is obvious: push rates down, push financial conditions looser, and keep the economy on overdrive (inflation be damned). It didn’t seem to make big news a couple of weeks ago, but the US Gov started to buy US Treasuries again (aka “Quantative Easing”) thus increasing the money supply, artificially keeping bond rates low, and likely putting downward pressure on the USD.

The other big piece of this is trade. Statistics Canada reported that Canada recorded a goods trade surplus of $153 million in September 2025, after a large deficit the month before. Trade surpluses don’t automatically make a currency rip higher overnight. But they do matter on the margin because they support underlying demand for Canadian dollars over time – especially if energy and commodity exports don’t fall off a cliff.

Despite the tariffs, the US still remains in a negative trade balance as we head into 2026. That’s not likely to change any time soon.

If the Loonie strengthens in 2026, it won’t feel like “good news” to everyone. It’s great if you’re booking U.S. travel or buying U.S. goods. It’s less fun if a big chunk of your portfolio is unhedged U.S. equities, because CAD strength can reduce your returns when you translate back to Canadian dollars.

Tesla Double Down

Last year, I put a big red circle around Tesla and said, at some point, the math would catch up with the story.

At the time, the logic felt straightforward. Tesla was trading at a valuation that implied it would eventually make more money than every other major car manufacturer combined. That never made sense to me then, and it makes even less sense now (especially since Tesla’s P/E ratio is 320x)!

To recap the original thesis: Tesla’s market cap versus industry profits was wildly out of sync. Sales were already slowing in key international markets. Competition was accelerating. Subsidies were under pressure. And Elon Musk was increasingly distracted.

None of that has meaningfully changed.

What did change is how investors decided to think about Tesla! Musk’s political adventures have completely crushed Tesla sales amongst environmentally-conscious Democrats (core supporters in the past) and his European comments have cratered brand value on that rapidly-electrifying continent.

Increased competition – particularly from companies like BYD – has eaten into Tesla’s once-dominant position outside North America (as I predicted last year). And political backlash against EV incentives has made the demand picture messier, not cleaner.

If Tesla were still being valued primarily as a car company, I’m comfortable saying the stock would be far lower today. What I underestimated was Elon Musk’s ability to change the narrative faster than the fundamentals could matter. Tesla is no longer priced as a car company. It’s priced as a vaguely defined artificial intelligence, robotics, autonomy, and “future tech” platform – one that can shift its story whenever the old one stops working.

And to be fair, Musk has always been an elite salesman.

The market didn’t punish Tesla for slowing car sales. It rewarded Tesla for suddenly turning itself into “not a car company.”

But I remain quite skeptical. Stories are powerful stock price movers in the short term. But eventually, math matters.

Right now, Tesla’s valuation assumes massive success in areas that are still largely unproven at scale. Autonomous driving. Robotics. AI-driven platforms. All of it might work… eventually But none of it is generating cash flows that justify today’s price.

I’m not predicting bankruptcy, but with the gap between narrative and cash flow wider than ever, I think Tesla shares will be down more than 30% at some point in 2026.

Oil Stays Below $63 Per Barrel

You know what doesn’t need oil? Data centres!

I don’t see the demand and supply realities changing all that much for oil in 2026.

Last year, I argued crude would stay capped below about USD $75 a barrel – and it mostly did. The market forces that kept prices contained then haven’t gone away. If anything, the setup heading into 2026 looks even less supportive of a sustained breakout.

Economies aren’t growing at a fast pace (especially if one considers the Chinese slowdown) and “drill baby drill” just seems to keep pumping more crude into world supply. US production remains near record levels. Every time OPEC+ signals restraint, American producers quietly pick up the slack. That dynamic makes it very hard for prices to stay elevated without deep and prolonged cuts from major exporters.

If we think there’s an outside shot that the Russia/Ukraine war could end, and/or that Venezuela might suddenly capitulate, we could see even more supply rush into the markets.

AI and USCMA – I Have No Idea

f I’m being completely honest here with my crystal ball, I have to admit that things are cloudy when it comes to the two biggest stories for 2026 (at least through a Canadian lens):

1) AI

2) USCMA/CUSMA (can we just call this NAFTA again?!!) negotiations

The AI story is so unique and so complicated, that I have no idea how it will play out in the next 12 months. I took my best stab at it a few weeks ago when I wrote about the AI bubble. I keep waiting for signs that this broad productivity mega-boost is upon us – and I’m just not seeing it.

Sure, AI is letting us be slightly better at a lot of things. Great. But like… this isn’t the first time we managed to harness electricity!

Even if AI can suddenly make the leap (maybe one day soon it will be able to draw a hand or a clock) I’m not at all sure that the big US companies are going to win vs the Chinese companies. AND, even if they do win, I don’t see any evidence that there will be some kind of thick profit margin there.

I have yet to see anyone refute the argument that if the Chinese AI companies are able to use cheaper electricity, cheaper labour, cheaper (non-tariffed) building materials – then why will they not be able to cut the legs out of any American AI developer when it comes to price to the consumer?

Then we get to the issue on the minds of so many Canadians: What is going to happen to Canada-US trade?

(Which – just to be clear – is… almost all of our trade.)

I wish I knew.

I was pretty sure last year that the Trump Regime was going to mess up world trade by putting tariffs on everyone (didn’t realize that would include penguins). I didn’t anticipate that most countries around the world would capitulate so quickly and not begin a spiralling trade war. While that’s pretty good news overall, it’s not great for specific industries in Canada.

There are so many variables to consider when it comes to what direction this all could take. Will it matter if the Supreme Court decides a lot of these tariffs are illegal (I don’t think it will matter much at all)? Will it matter that just as we sit down to negotiate, Trump is likely to be losing power by the day due to the midterms fast approaching (and the fact his policies are pretty awful)? We’ve got a new ambassador – does that matter? Will American business leaders suffering from uncertainty and consumers suffering from tariff-driven inflation push hard enough that someone pays attention to them?

It’s all so confusing – especially when you consider how fast this administration changes its mind on these issues.

Good News for 2026?

So I have to admit, as I re-read my predictions for 2026 I’m not seeing a lot of good news here as far as Canadian investing goes.

There are definitely some good things happening for Canadians – they just might take a little while to come to fruition.

I think the Carney government has taken meaningful steps to help the economy grow. Home prices have moderated a bit relative to wages in Canada – which is great to see.

Prices on Canada’s best ETFs continue to trend downward (thanks Vanguard)!

Maybe AI really will live up to its promise and start a never-ending abundance loop!

And hey, an investor has to be thankful for the incredible returns over the last three years. Any lukewarm or even pessimistic stock price predictions have to be put into the context of experiencing one of the most incredible periods of wealth creation we’ve ever seen!

Maybe that continues unabated in 2026. But for now, I’m not getting my hopes up too high.